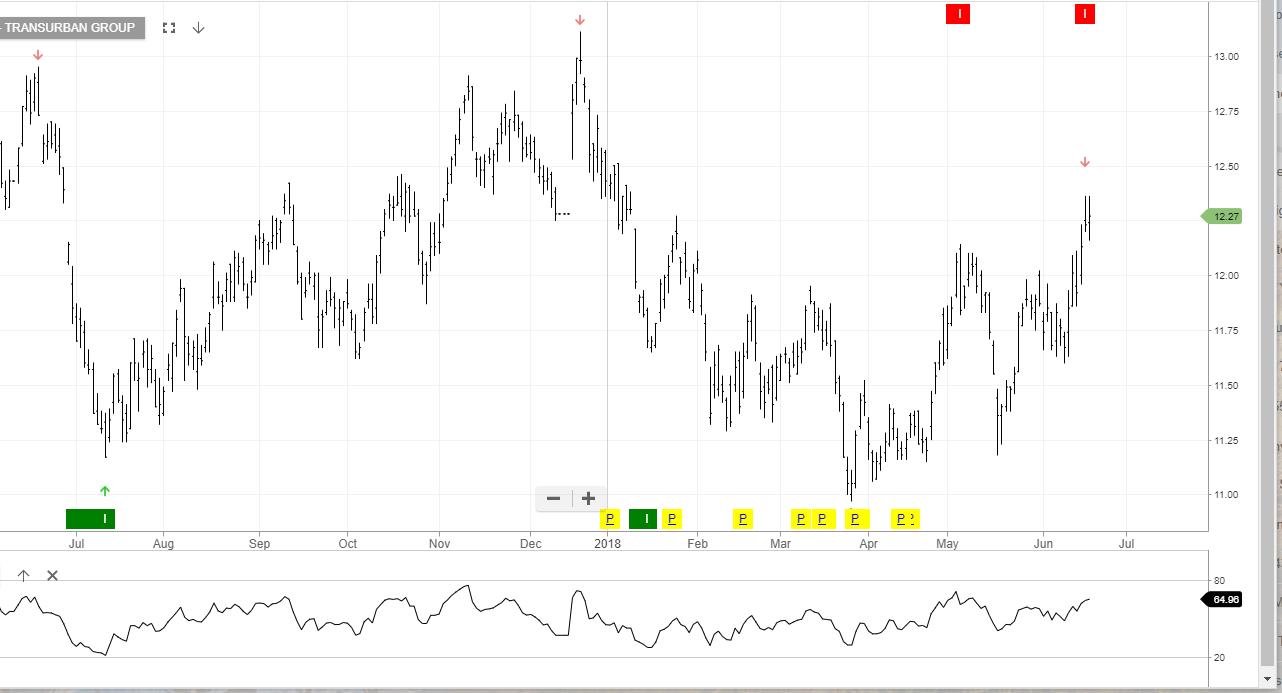

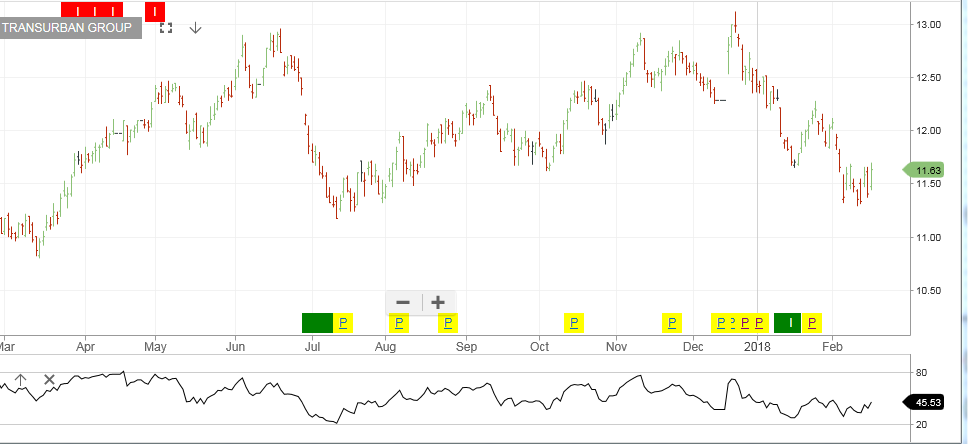

Enhance Cash Flow On TCL And SYD

Our ALGO engine triggered a sell signal on both SYD and TCL into yesterday’s ASX close at $7.47 and $12.20, respectfully.

We suggest either taking profits on the stock or using the option strategy outlined below.

With both of these names going ex-dividend on June 28th, we suggest selling a call option above the market to increase cash flow and enhance the return.

For TCL, we are looking to sell the October $12.50 call for around 24 cents and collect the 28 cent dividend.

For SYD, we will sell the October $7.75 call for around 12 cents, which will keep investors in the stock to collect the 18.5 cent dividend.

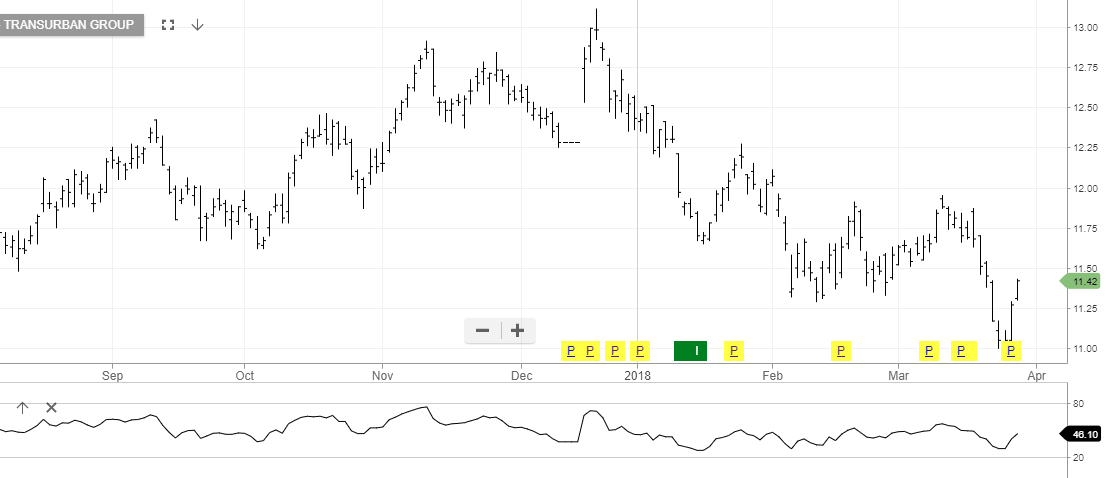

Transurban

Sydney Airport

Sydney Airport

Sydney Airport Transurban

Transurban