Has The AUD Reached The RBA’s Pain Level?

At the start of the year, the market consensus was for the Aussie Dollar to fall against the major currency pairs during 2017. So far this year, the AUD/USD has climbed 10% and almost touched .8000 last week.

At 1pm today, RBA chief Philip Lowe will be giving a speech in Sydney. Since many exporters look at .8000 as a pain level, it’s reasonable to expect Mr Lowe to comment about the level of the Aussie.

The strengthening AUD/USD has created a headwind for domestic companies with earnings exposed to the softening USD.

Four companies that we follow which have seen their share prices dampened due to a stronger Aussie are: BXB, CPU, ANN and JHX.

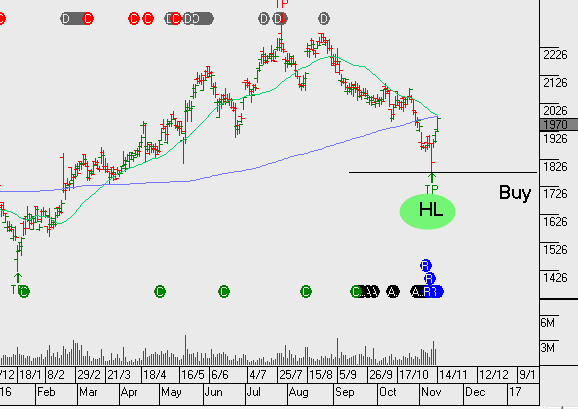

Australian Dollar

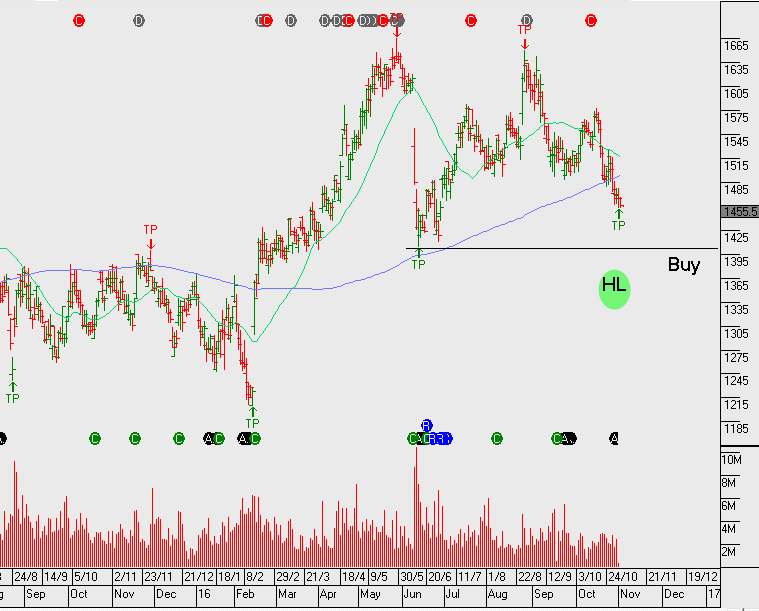

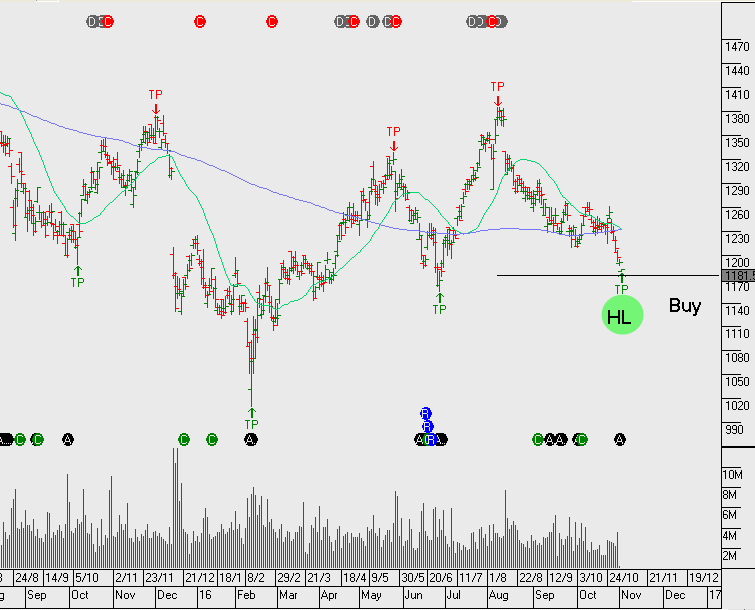

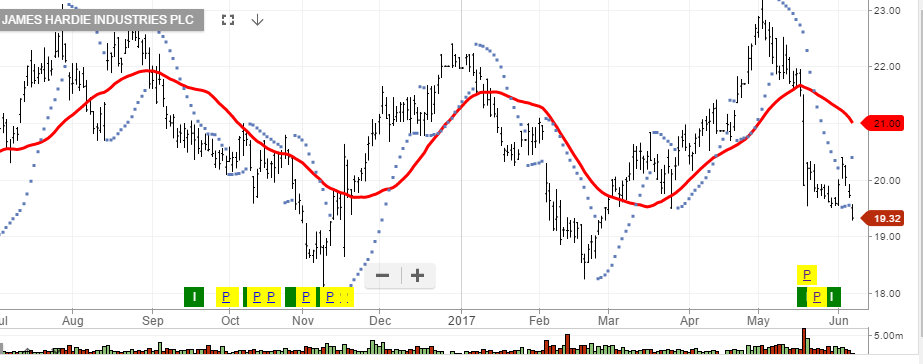

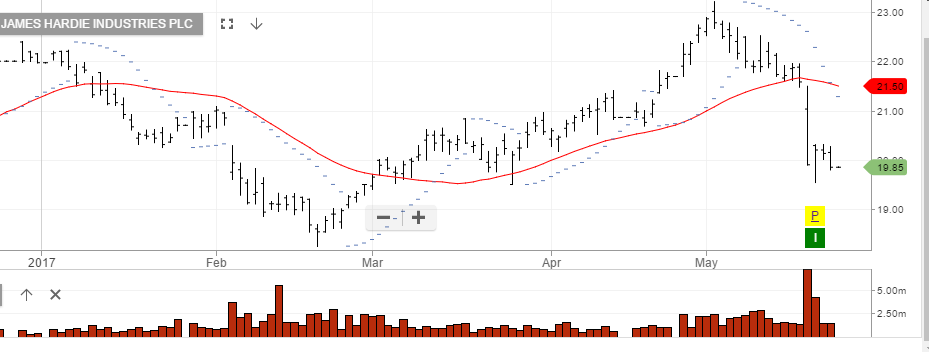

James Hardie

James Hardie James Hardie

James Hardie