Banks Reverse Levy-Related Plunge

Shares of the major banks dropped sharply at yesterday’s open as budget-related fears triggered intra-day volatility rates not seen in the banking names for over 2 years.

Prices rebounded throughout the trading session in what we consider technical , value-related buying, which substantially pared the early losses.

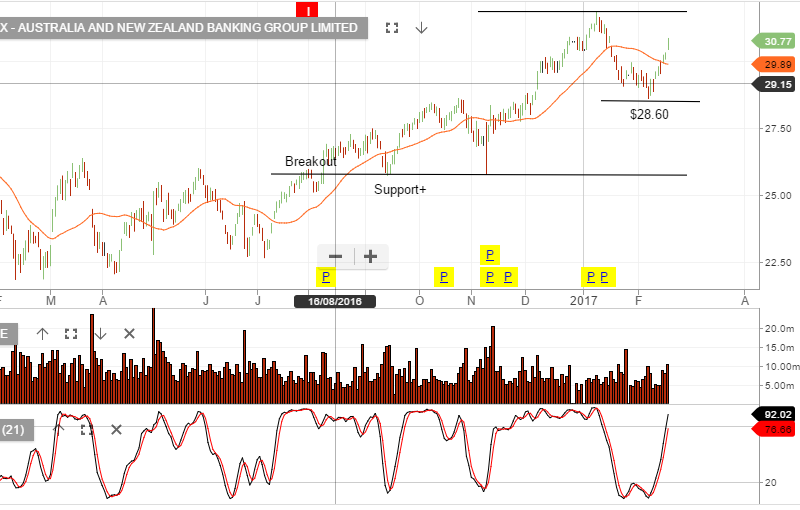

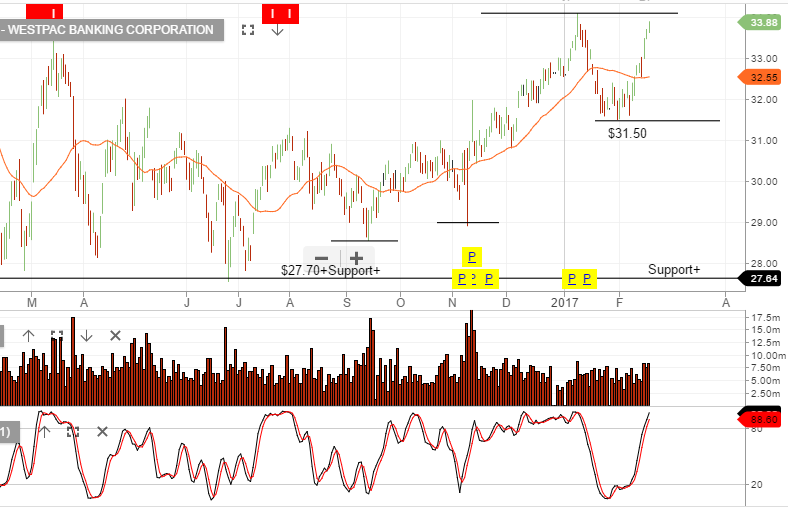

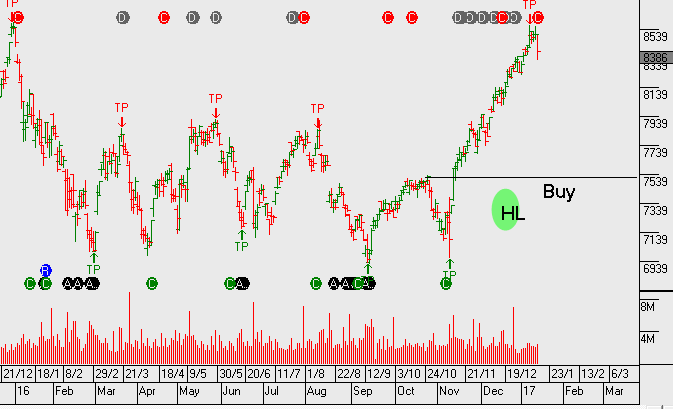

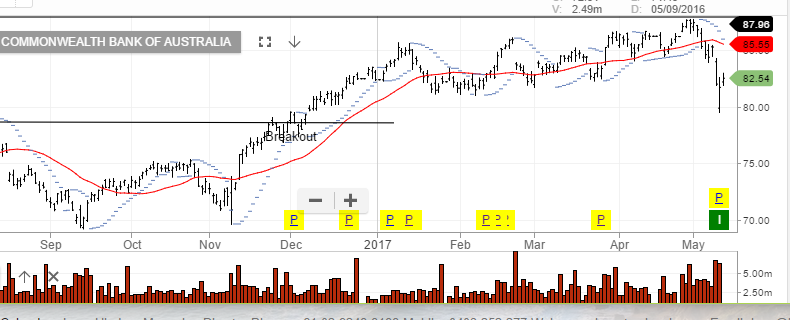

The strong reversal in share prices triggered the ALGO engine to give buy signals in ANZ, CBA, WBC .

Given the murky outlook for earnings growth, and increased bad-loan provisions across the banking sector, we only expect the recent price action to form a 50% retracement of the recent losses, at best.

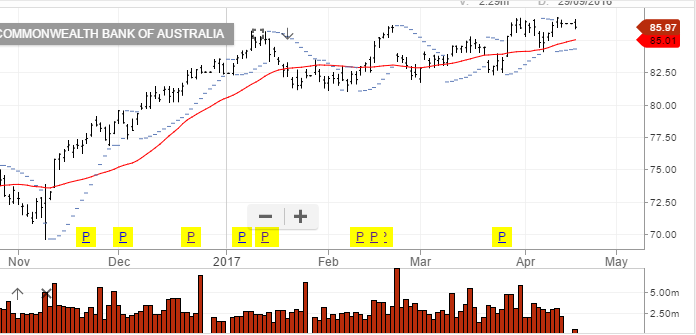

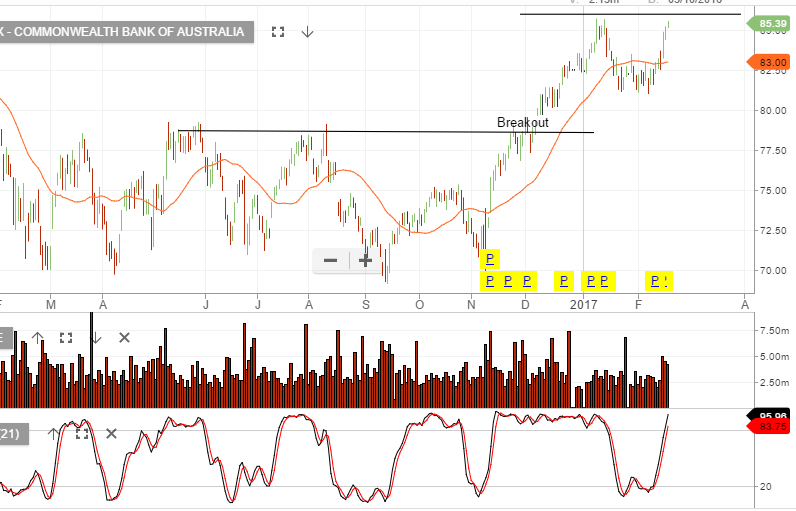

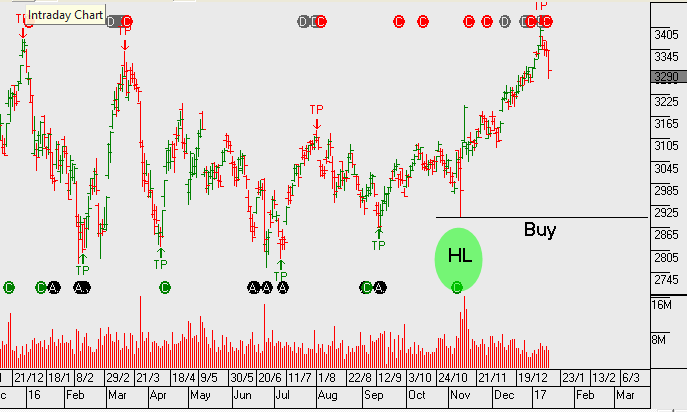

Commonwealth Bank