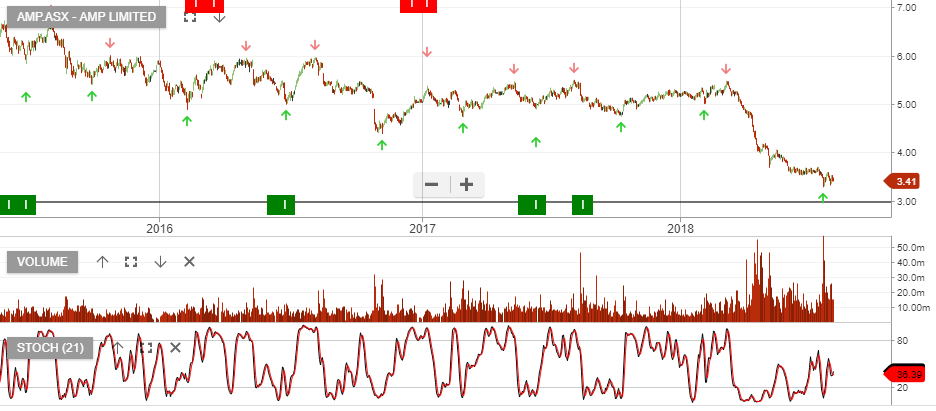

AMP

AMP is added to our watchlist, and we’re now waiting for the price action to cross above the 10-day average.

AMP is added to our watchlist, and we’re now waiting for the price action to cross above the 10-day average.

AMP is rated a buy at $1.42.

AMP remains an overweight multi-year recovery play.

AMP is growing earnings at 5%+ and delivering new product innovations that support our buy rating.

AMP is likley to deliver imroved earnings growth in FY24 & FY25.

AMP has built a higher low formation with support at $0.91.

AMP is a current holding in our Trade Table.

AMP’s 1H18 result was underpinned by effective cost management offsetting

weaker revenue performance.

The Australian Wealth Management division saw net outflows of $673m in the quarter.

Going forward, we expect well managed costs to offset weaker revenue. There is longer-term value here for patient investors, who are willing to hold the stock through to the appointment of a new permanent CEO.

In 2019, AMP’s board will likely outline a plan to split the funds management business away from the traditional advice side model, unlocking value for shareholders.

We have AMP now trading on a 6.8% yield and expect FY19 reported profit to remain around $800m.

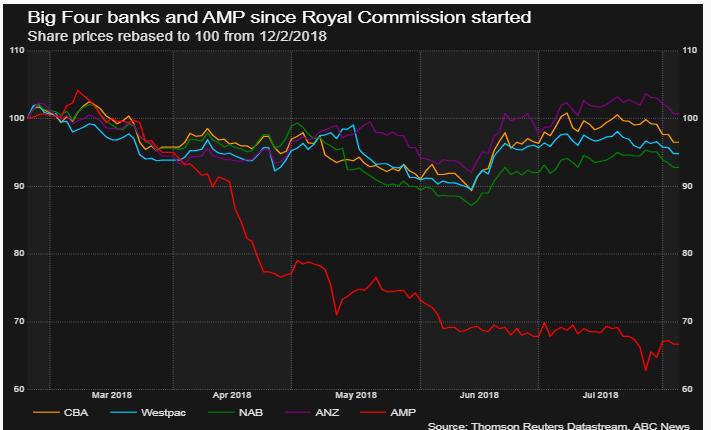

AMP

The Big four banks will be in the spotlight this week as the Banking Royal Commission commences round five today in Sydney.

The main topic for this round of examination will be the fees, charges and weak performance of bank-managed superannuation funds.

One Melbourne-based think tank has estimated that excessive fees and poor performance can cost superannuation investors up to $12 billion per year.

Australia’s largest superannuation provider, AMP, felt the wrath of the Royal commission during the last round of testimony, which saw their share price drop over 30% and the sacking of its chairman, CEO and three other directors.

The chart below illustrates the performance of AMP’s share price relative to the other Big 4 banks.

We don’t have ALGO buy signals for any of the domestic banks and we’re not holding any banking names in our ASX Top 100 portfolio. However, we will look for signals as the share prices approach the June lows.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Or start a free thirty day trial for our full service, which includes our ASX Research.