Rio Tinto

Rio Tinto is a new position in our ASX 200 Trade Table.

Rio Tinto is a new position in our ASX 200 Trade Table.

VanEck Vectors China New Economy is oversold and offers investors an attractive entry point.

South32 is under Algo Engine buy conditions.

Global X Semiconductor is rated a buy on a deeper pullback into the $13 – $15 price range.

NAS:PLTR remains on track to become a leader in the AI software industry.

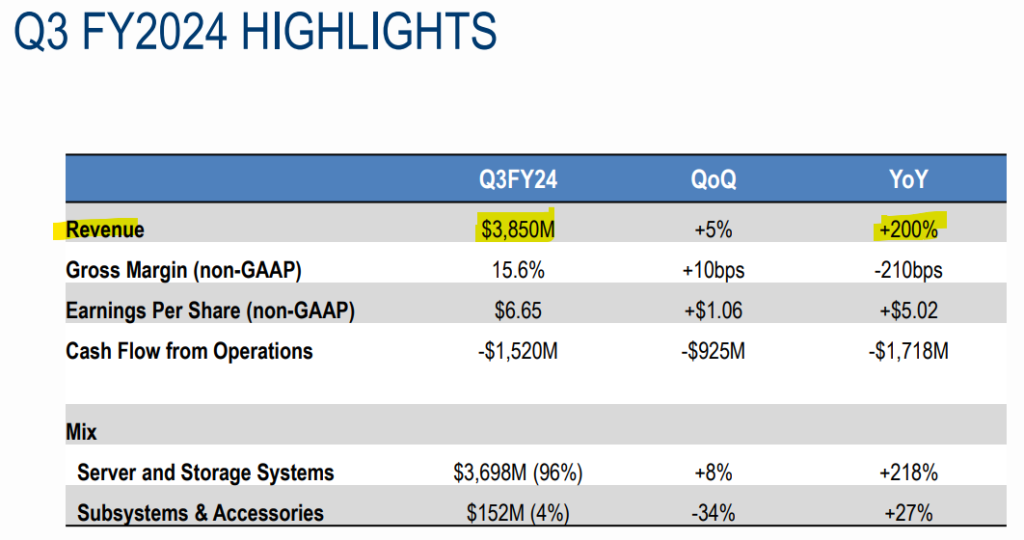

Super Micro Computer, trades on a forward PE of 30x earnings. The June 2024 earnings release is scheduled for 6 Aug.

Super Micro Computer develops and manufactures high-performance server solutions, vital for data centers that power LLMs.

Last quarter results.

Week 3.

Monday, July 29 – McDonald’s, ON Semiconductor, and Welltower.

Tuesday, July 30 – Microsoft, Procter & Gamble, Merck, Advanced Micro Devices, Pfizer, Starbucks, and S&P Global.

Wednesday, July 31 – Meta Platforms, Mastercard, Qualcomm, Western Digital Corporation, Arm Holdings, Boeing, eBay, Altria, Marriott International.

Thursday, August 1 – Amazon, Apple, Intel, Block, DoorDash, Cigna, ConocoPhillips, Anheuser-Busch InBev, Roblox, and DraftKings.

Friday, August 2 – Church & Dwight, Chevron, and Exxon Mobil.

Week 2.

Monday, July 22 – Verizon Communications and NXP Semiconductors.

Tuesday, July 23 – Alphabet, Tesla, Visa, The Coca-Cola Company, Texas Instruments, Philip Morris International, United Parcel Service, Lockheed Martin, General Motors, and Comcast.

Wednesday, July 24 – International Business Machines, AT&T, Chipotle Mexican Grill, General Dynamics, and Ford Motor.

Thursday, July 25 – AbbVie, Northrop Grumman, Union Pacific, and AstraZeneca.

Friday, July 26 – Bristol Myers Squibb, Colgate-Palmolive, and Charter Communications.

Week 2.

Monday, July 15 – Goldman Sachs and BlackRock.

Tuesday, July 16 – UnitedHealth, Bank of America, Progressive, Morgan Stanley, PNC Financial, and J.B. Hunt Transport.

Wednesday, July 17 – Johnson & Johnson, U.S. Bancorp, Kinder Morgan, United Airlines, and Ally Financial.

Thursday, July 18 – Netflix, Abbott Laboratories, Blackstone, Domino’s Pizza, and Taiwan Semiconductor Manufacturing.

Friday, July 19 – American Express, Halliburton, and Traveler.

Week 1

Thursday, July 11 – Delta Air Lines, PepsiCo, and Conagra Brands.

Friday, July 12 – Citigroup, JPMorgan Chase, Bank of New York Mellon, and Wells Fargo.

VanEck Vectors MSCI Inter Small Companies QUAL Financial, industrial, and staples shares have largely outperformed tech. And small caps have rallied 10 percent.

Ramsay Health Care is rated as a buy with a stop loss at $46.30

Our current ASX 200 Trade Table holdings include…

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Or start a free thirty day trial for our full service, which includes our ASX Research.