There are new Signals.

For our Members, please find below the latest list of signals.

For our Members, please find below the latest list of signals.

ASX:CFK is a buy at $9.45 with a stop loss t $8.97.

Northern Star Resources is a buy with a stop loss below the $14 support level.

Ramsay Health Care is under Algo Engine buy condition.

ASX is under Algo Engine buy conditions.

Aurizon Holdings is rated a buy, and we suggest a stop loss at the $3.64 pivot low.

For our Members, please find below the latest list of signals.

On April 25, 2024, Intel reported its Q1 FY24 earnings with revenue of $12.7 billion, a 9% increase YoY, and non-GAAP EPS of $0.18, both beating Wall Street expectations. However, the revenue guidance of $12.5 billion to $13.5 billion fell short of Wall Street’s expectation of $13.63 billion, leading to a plunge in the stock price to around $30 per share.

Intel is a high-risk recovery play in the chip space. We consider the current share price to be at an inflection point, and it will begin to rise in mid-to-late 2024. The first positive catalyst is the US government’s CHIPs Act funding payment. A multi-year recovery should follow, driven by innovation and AI data center sales.

Sonic Healthcare advises that it is now forecasting EBITDA for FY 2024 of approximately A$1.6 billion on revenues of approximately $8.9 billion. Revenue growth continues to be strong at 6% for the 4 months to 30 April 2024 (following 6% in H1 FY 2024). However, profit growth has been lower than expected, in part due to inflationary pressures on the business, and exacerbated by currency exchange headwinds. In addition, a number of margin improvement initiatives planned for completion in H2 FY 2024 have been slower to deliver than expected and will contribute to further earnings growth in FY 2025. The inflationary pressures are expected to ease going forward, with headline inflation rates in Sonic’s main markets already reduced to a range of 1.4% to 3.6%.

Based on preliminary forecasts, on a FY 2024 forecast constant currency basis, Sonic expects to

achieve EBITDA of approximately A$1.70 – 1.75 billion in FY 2025. Guidance for FY 2025 will be updated/confirmed at Sonic’s full year results’ release in August 2024.

Sonic Healthcare’s CEO, Dr Colin Goldschmidt said: “The 2024 financial year has been one of

transition for Sonic Healthcare, moving away from pandemic conditions into a more normal business

environment. Our current robust topline growth, organic and non-organic, in a setting of inflationary

cost pressures, have combined to delay the completion of our programs to align labour costs more

closely with post-pandemic conditions. These unique business conditions have also made forecasting

our earnings unusually difficult this year. FY 2024 has also been a year of investment for future growth. In particular, the sizeable acquisitions of SYNLAB Suisse and Dr Risch (Switzerland), PathologyWatch (USA) and the Hertfordshire & West Essex contract win (UK), while initially earnings and/or margins dilutive, will all yield strong earnings growth and returns on investment into the future.

“Overall, the company remains in a very strong position, both financially and in terms of market

positioning. We remain well set for growth in revenues and earnings going forward, including realising

over the next two years the synergies and enhanced returns from the investments made this year. In

managing our costs, especially labour costs, we have been mindful to protect our brands and to support

our ongoing strong growth and the high quality of essential services we provide.”

Shopify Inc. Class A Subordinate Voting revenue is expected to grow by 20% to $8.5 billion in 2024. Currently trading at 8.8x estimated sales, Shopify remains undervalued relative to its software and e-commerce peers with a similar growth profile.

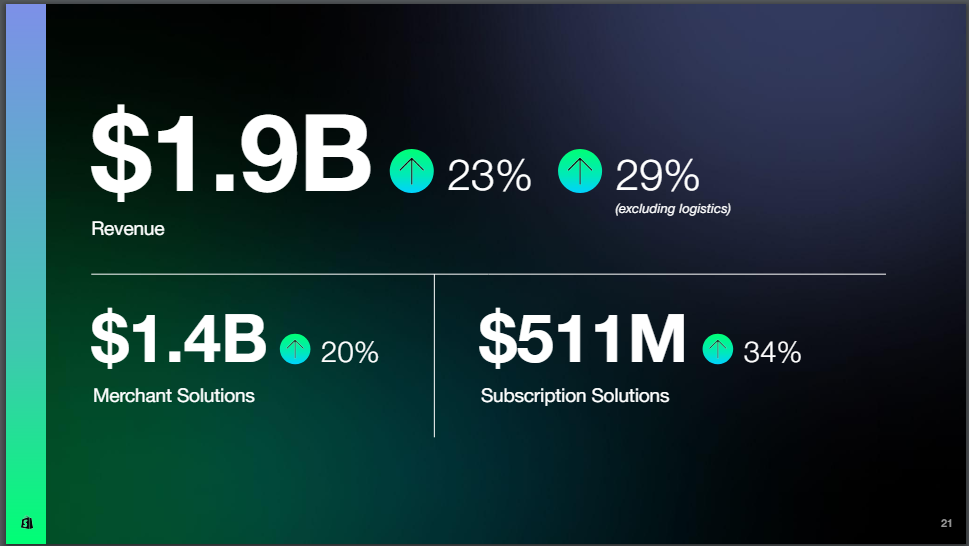

We rate SHOP a buy within the $50 – $60 price range.

Q1 2024 revenue increased 23% to $1.9 billion compared to the prior year, which translates into year-over-year growth of 29% after adjusting for the sale of our logistics businesses

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Or start a free thirty day trial for our full service, which includes our ASX Research.