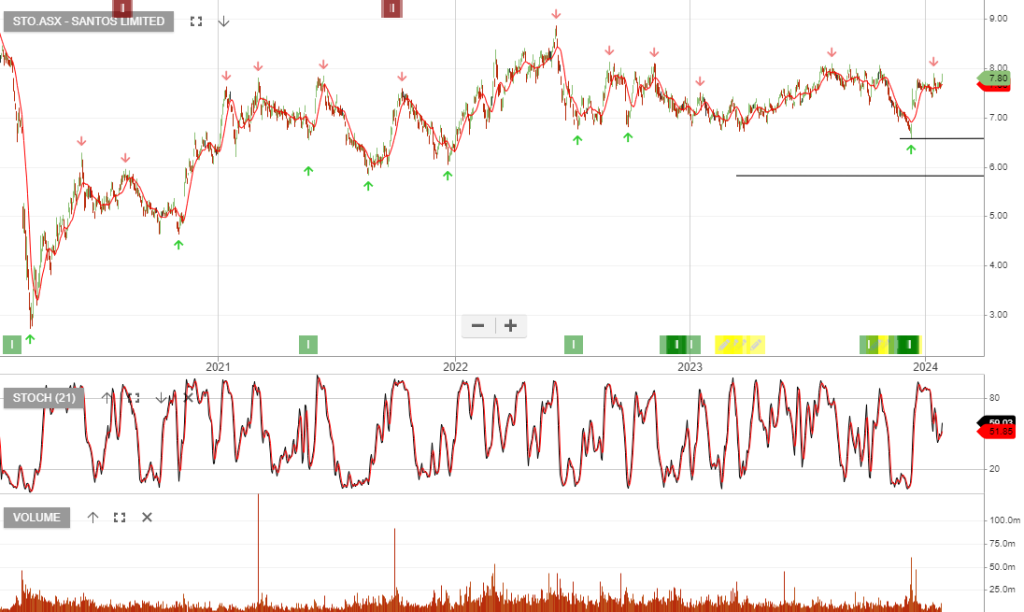

STO shares remain heavily discounted, given superior free cash flow. Barossa project progression, completion of PNG selldown, and the potential merger proposal from WDS are all positive catalysts.

We expect STO to report a solid 4Q on 25th January and we look to buy STO on the current dip in price.