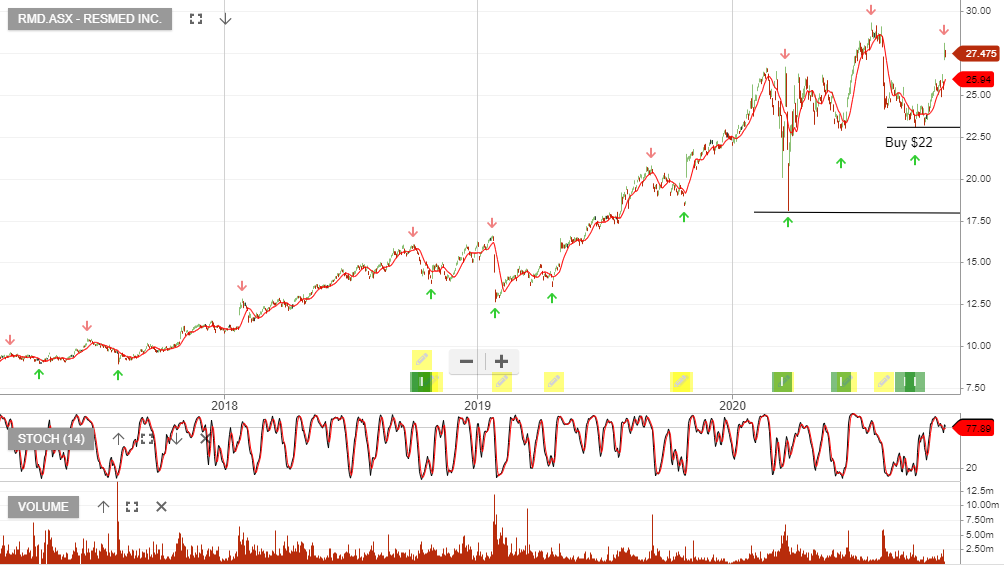

ResMed is under Algo Engine buy conditions and is a current holding in our ASX model portfolio.

Resmed reported better than expected 1Q21 earnings with group revenue up 10% and NPAT up 37% on the same time last year.

At 35x PE Resmed remains expensive and will need to maintain double-digit earnings growth to sustain the current valuation.

Buy on future share price weakness.