Orica is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

FY21 revenue is likely to remain flat at $5.8bn and EBIT is forecast to increase 3-5% to $630mn. This supports a forward yield of 2.8%.

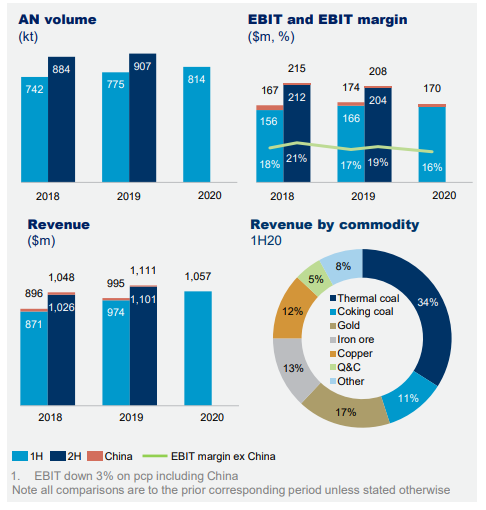

Earnings are likely to be well supported due to higher volumes and the strength in the mining industry, especially from the gold mining market.

Earnings may surprise to the upside and we continue to hold ORI into the next earnings release.