GPT – High Conviction Buy

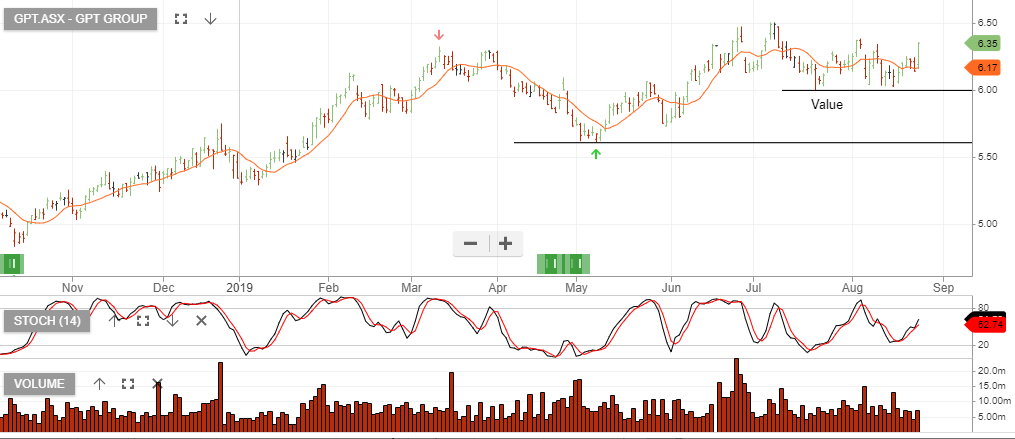

GPT remains a high conviction buy. The share price has rallied 5% over the past week and we now recommend selling covered call options to enhance the income return.

GPT goes ex div $0.13 on the 28th of December.

GPT remains a high conviction buy. The share price has rallied 5% over the past week and we now recommend selling covered call options to enhance the income return.

GPT goes ex div $0.13 on the 28th of December.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Crown Resorts is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

The group announced its results for FY19 with NPAT down 5% to $370mn. A final dividend of $0.30 cents was declared.

Despite the short-term headwinds from lower VIP revenue, we see value in Crown shares as investors are effectively getting free upside in the Barangaroo project.

Buying support at $11.00

Origin Energy is a holding in our portfolio, based on the strong anticipated earnings coming from the group’s investment in the Australia Pacific LNG project.

The result announced today shows an increase in profit from the APLNG of 40% plus. Overall group earnings are ahead of market consensus at $1bn and the company declared a $0.15 dividend.

Coles Group is under Algo Engine buy conditions and is now a holding in our ASX 100 model portfolio.

FY19 profit fell 9% to $1.43b, which was down from $1.58 the previous year.

The company declared a final dividend of $0.24 and a special dividend of $0.115.

We see support for the share price at $13, underpinned by the extensive cost-cutting program announced in the last quarter. Target cost savings over the next 3 – 5 years exceed $1 billion dollars.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sonic Healthcare is under Algo Engine sell conditions, however, we take the time to look at the financial outlook of the business, following yesterday’s FY19 result.

FY19 sales revenue was up 11.6% and EBIT growth increased by 10%.

Excluding any FX benefit, we expect Sonic to grow FY20 EBITDA at 6 – 8%, which will support a forward yield of 3.2%.

The stock is trading on FY20 PE of 23x earnings and we will look to buy SHL on the next Algo Engine buy signal.

Seek is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

The company reported its FY19 earnings yesterday and provided strong guidance and a positive outlook for FY20.

F19 was in line with consensus with revenue up 18% and EBITDA up 8%.

FY20 guidance has been upgraded to 15 – 18% revenue growth and profit growth of 10%+. Seek now trades on a 2.8% forward yield.

Buy Seek and sell out of the money covered calls to enhance the yield.

BHP Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

The company announced its FY19 earnings, which were in line with consensus expectations. Operating costs are slightly elevated but high iron ore prices will offset this in FY20.

FY19 reported EBITDA US$23.2bn and underlying attributable profit of $9.1bn. The market was disappointed that no buyback was announced but BHP did declare a final div of US$0.78 per share.

Total dividends for the year were US$1.33 per share, based on 74% payout ratio.

FY20 revenue is forecast to be $48bn, EBIT $19bn, net profit $11.5bn, which will place the stock on a 10x PE multiple and a forward yield of 6.5%.

We see value support for BHP & RIO near the current price range.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Or start a free thirty day trial for our full service, which includes our ASX Research.