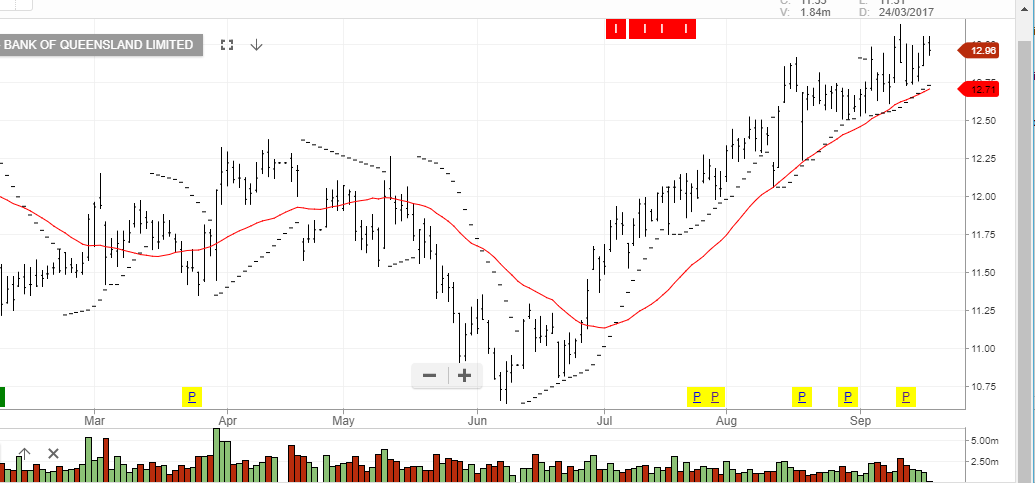

In a recent analyst review, the forward pricing on BoQ has been gauged at 12% overvalued and adjusted lower from current levels to $11.50 over the medium-term

The note focused on the bank’s balance sheet being skewed towards residential mortgages and that a rise in bad debts will put downside pressure on operating margins.

We agree with the initial downside target of $11.50 and see scope for some range extension into the low $11.00 handle.

Bank of Queensland

Bank of Queensland