Boral intends to acquire US based building product group Headwaters Inc in a deal worth US$2.6b The transaction has been approved by the Headwaters’ Board and is expected to close mid next year.

Boral will raise $2b through a $1.6bn retail and institutional entitlement offer and a A$450m institutional placement at an issue price of $4.80 per share. The remaining $1.6b will be funded through existing cash and debt.

We continue to see upside in Boral & James Hardie.

Crude Oil prices rallied over 4% to a three week high today, as the market perceived a growing conviction that major oil producing countries would agree to limit output at the OPEC meeting in Vienna on November 30th.

West Texas Intermediate crude oil traded as high as $48.50, up over 10% in five days, since Saudi Arabia, the de facto leader of OPEC, increased pressure on the group’s more reluctant members to join its proposed reduction of output plan. In recent days, OPEC members including Iran, along with non-OPEC member Russia, have suggested that they were leaning toward a deal to limit production.

Both Iran and Russia have been the main hurdles facing any output curtailment by OPEC, as both nations want exemptions to try to recapture market share lost by years of Western sanctions. Analysts have been clear participation by Iran, Nigeria and Libya are integral in any agreement to cut production and shore up crude oil prices.

There is a saying in the financial markets that a “rising tide floats all boats” This old adage has been used recently to describe how the rally in US bank shares has lifted the share prices of Australian banks.

Since November 4th, shares of Citibank have gained 14%, shares of JP Morgan have gained 16%, shares of Bank of America have risen by 17% and Goldman Sachs shares have rallied by over 20%.

Over the same period of time, shares of ANZ have gained 6%, shares of Westpac have gained 8%, CBA shares have lifted by 8.5% and shares of the NAB have rallied by 11%.

Interest rates in the US began bottoming out in late September, which was positive news for most US financial names. In addition, the election of Donald Trump is being hailed as a “game changer” for the U.S. banking sector, as the Republican sweep of the White House and both houses of Congress appears to have shifted investor’s expectations about interest rates, regulation and the broader business environment.

With respect to the Australian banking names, these two key points aren’t applicable.

The RBA may have moved to a neutral bias on domestic interest rates, but there’s no realistic expectations for a rate hike anytime in the foreseeable future. And, if any regulatory changes are legislated in the Australian banking industry over the next 12 months, they are more likely to be restrictive, as opposed to accommodative.

With this in mind, we will use this recent rally in Australian banking names to implement our derivative overlay strategy and sell covered call options to enhance returns on bank share holdings.

Stay tuned to the Investor Signals daily blog for specific timing and price information.

The sell-off in property trusts and infrastructure names has been substantial, 15 to 20% since early September.

The REIT sector has underperformed as bond yields have rallied. The repricing has seen the dividend yield of REIT’s back above 5%.

Historically, the correlation between Australian yield names and US 10-year yields has been inverse; as US yields fall, Australian property trusts and infrastructure stocks rise.

US 10-year bond yields have risen by 79 basis points, or over 50%, since early October. We see this pace as unsustainable and expect the local yield names to trade higher as the US Treasury yields drift lower.

We continue to track WFD, GPT, SGP, SYD and TCL versus the US10 year bond yields.

Federal Reserve Chief Janet Yellen was on Capitol Hill today addressing Congress for the first time since the US Presidential election. With the USD Index pushing against a 13-year high over 101.00, it was reasonable to expect some of her testimony to address the stronger USD and the sharp increase in Treasury yields. However, these specific developments weren’t addressed and, instead, Ms Yellen expressed confidence in the progress the economy is making towards their inflation and employment goals.

She indicated that waiting too long would force the FED to tighten faster in 2017 and could spur excess volatility in financial markets, but gave no indication about the pace of interest rate normalisation going forward. On balance, her comments were hawkish enough to keep the G-7 basket of currencies under pressure against the USD, but tempered enough to lift the DOW Jones 30 and SP 500 back up into historic high closing territory.

The economic data released supported this view with housing starts and building approvals rising sharply and weekly jobless claims falling to a 40-year low at 235,000. With three other FED Governors scheduled to speak today, we could see further confirmation that US rate policy is ready to adjust higher.

With all of the bullish USD data stacking up, it’s no surprise that the EUR/USD made a new low for the year, fell for the 9th consecutive day and posted a NY close below 1.0650. It’s worth noting that only once in its 17-year lifetime has the EUR/USD gone down 9 days days in a row. That was from August 28th to September 11th, 2008 when the pair dropped for 11 days in a row and lost close to 10 big figures from 1.4810 to 1.3880. The Euro also lost more ground against the Sterling, reaching a 7-week low of .8540, which is more than 11.5 big figures below the spike high of .9695 on October 6th.

With the Fed Funds futures now showing a 98% chance of a rate hike in December, we expect the chatter from the FED Governors to remain hawkish about the December hike but somewhat blithe about the dot plots and interest rate trajectory going into 2017. It was the markets’s expectation of 4 rate hikes in 2016 which roiled global equity markets earlier this year, and it’s unlikely that the voting FOMC members will want to repeat that level of market dysfunction.

With this in mind, we expect the USD to maintain an upward bias, but with a slower pace, and for US Stock indexes to probe higher and beyond recent resistance levels.

Currently ASX leading indices are building higher highs and higher lows and therefore, our predominate focus is on long or buy side signals triggered by the Investor Signals algo engine. When the structure of the indices turn bearish, we’ll provide greater analysis and coverage of short signals.

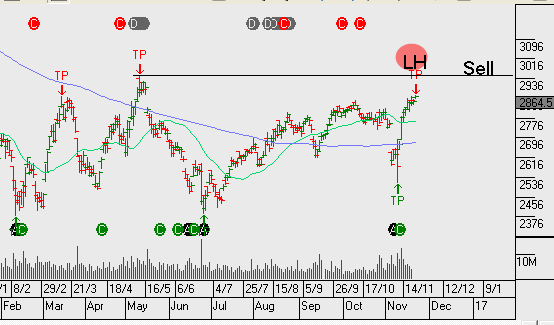

Occasionally, counter trend opportunities will present and work their way onto our radar screen. CPU and AGL are two countertrend short signals we’re monitoring.

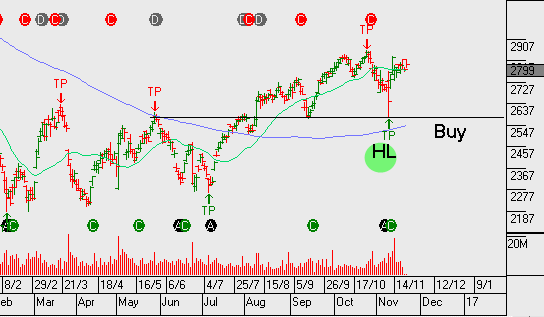

Our algo engine triggered a buy signal on Procter & Gamble (PG.NYS) overnight. We have added the stock to our watch list and look for an entry condition at or near $80

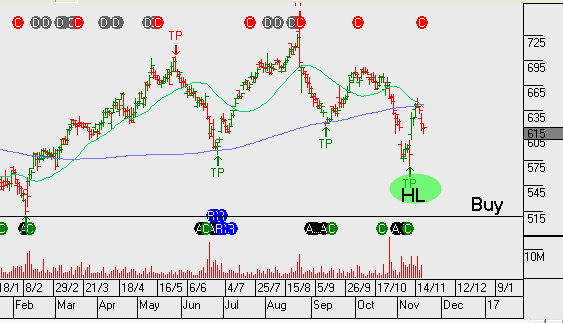

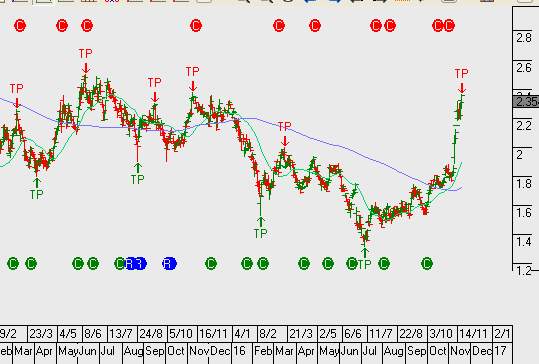

We’ve been buyers of SEK this week at or near $14.50. We highlight the benefit of running a stop loss as indicated on the chart. Whilst we see value at the current price point, we’re also mindful that the technical structure is weak, therefore, as a protection of capital we apply a stop loss at $13.90

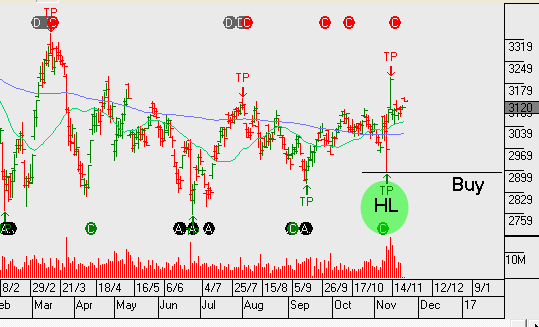

Seek (SEK.ASX) reported FY16 NPAT of $198m in line with guidance. The company maintained FY17 guidance of NPAT in the range of $215 – $220m.

Weakness in the education segment was off set by strength in the Asian employment business. FY17 revenue should increase 10% to $1b on EBITDA of $415m, EPS of $0.64 representing 15 – 20% underlying growth. This places the stock on a forward yield of 2.8%, assuming $0.40 in dividends for FY17.

Chart – Seek

Send our ASX Research to your Inbox

Or start a free thirty day trial for our full service, which includes our ASX Research.