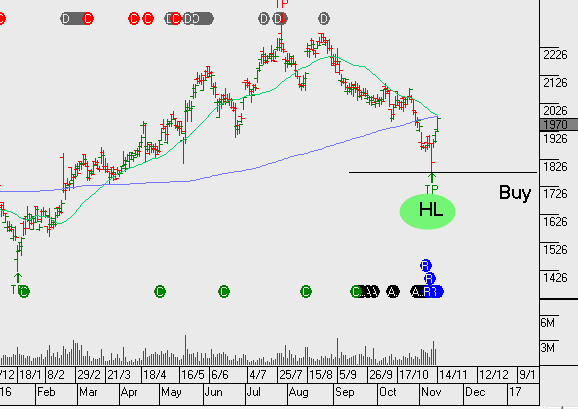

We recently highlighted James Hardie as a buy recommendation and we therefore draw your attention to the upcoming 2Q earnings result scheduled for release on Thursday.

Consensus expectation for FY17 net profit is around US$275m. This will mean JHX is delivering 15%+ EPS growth. It’s likely that a positive earnings trend can be supported by stronger demand for its products from North American consumers.

FY17 revenue $2b, EBIT $400m, NPAT $275, EPS $0.65, DPS $0.44 places the stock on a forward yield of 3%