Shares of Lockheed Martin closed 5% higher at $243.00 after the defense contractor beat Q3 earnings expectations.

The company reported adjusted earnings of $3.61 per share, well above the consensus of $2.89 per share. It reported sales of $11.55 billion, up from $10.06 billion in the year earlier period and above the consensus of $11.45 billion.

Lockheed said it expects overall 2016 earnings per share of $12.10 and sales of $46.5 billion, as adjusted for divested business. The company expects ongoing operations to lift 2017 net sales by 7%.

The strong price response was welcomed as shares of Lockheed have fallen 9% in the last three months from the August high of $264.00.

The price of Apple shares traded in a wide range after the company reported slightly better earnings but the lower quarterly results marked the third quarter of year-over-year revenue declines.

The iPhone maker reported earnings of $1.67 per share, just above the $1.66 expected consensus. Revenues came in at $46.90 billion, just shy of the 46.94 billion expected. That’s down from the comparable figure of $1.96 per share on sales of $51.5 billion a year ago.

Apple shares rose briefly to $119.00 in after hours trading, but were last seen down more than 2% and dipping below the mid-September support area at $115.00. The company reported that it shipped 44.8 million iPhones, which is down from 48.04 million a year ago.

Shares of Visa Corporation were down over 1% in after hours trade after a solid earnings report was followed by weak 2017 guidance.

The credit card provider beat Q4 forecasts of 68 cents by announcing an 18% rise in earnings to 73 cents per share. Q4 revenue increased by 15% to $4.23 billion against the same period in 2015. The better-than-expected Q4 growth was helped by its acquisition of Visa Europe.

However, fiscal 2017 adjusted earnings per share growth was estimated at just over 15% versus a consensus for a 19% increase, which pushed the stock lower. The September low of 81.30 will offer the first key support level.

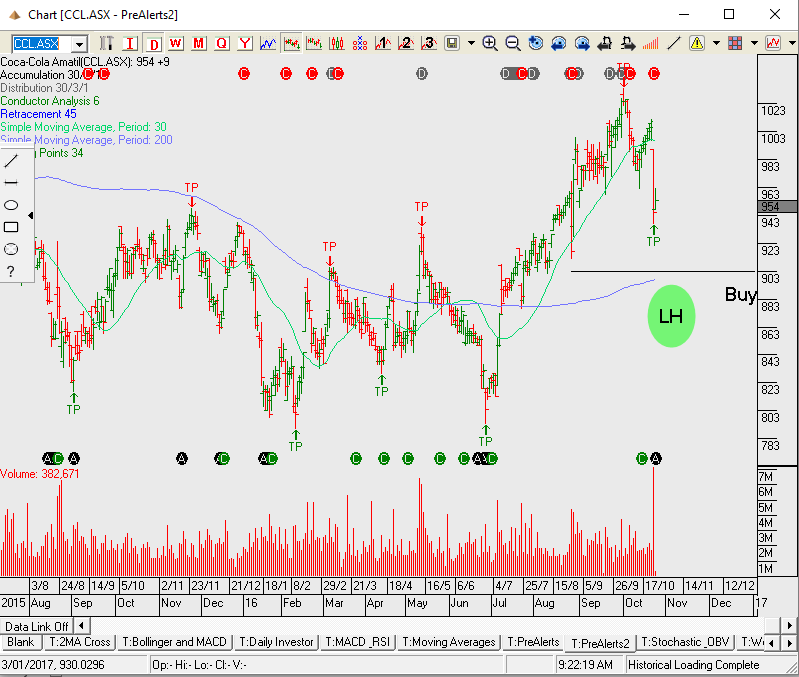

CCL has it challenges as consumer trends continue to move away from large volume consumption of carbonated sugar drinks. CCL is responding through new product ranges and reducing the size of both cans and bottles.

$100m in cost savings along with automation and efficiency gains in the production facilities will help to offset any revenue weakness. Our base case for CCL on a 12 to 24 month outlook is for relatively flat revenue and EPS growth.

FY17 revenue $5.2b, EBIT $680m, EPS $0.55, DPS $0.45 places the stock on a forward yield of 4.8% and a PE ratio of 17x.

We’ve been active in selling covered calls over CCL as we’ve maintained full value is around $9.50. Keep CCL on your radar as a pull back to $9.00 is worth considering as an entry point to buy the stock. We think CCL trades in a consolidation channel over the next 12 months. A combination of the dividend and option premium produces 10% annualised cash flow.

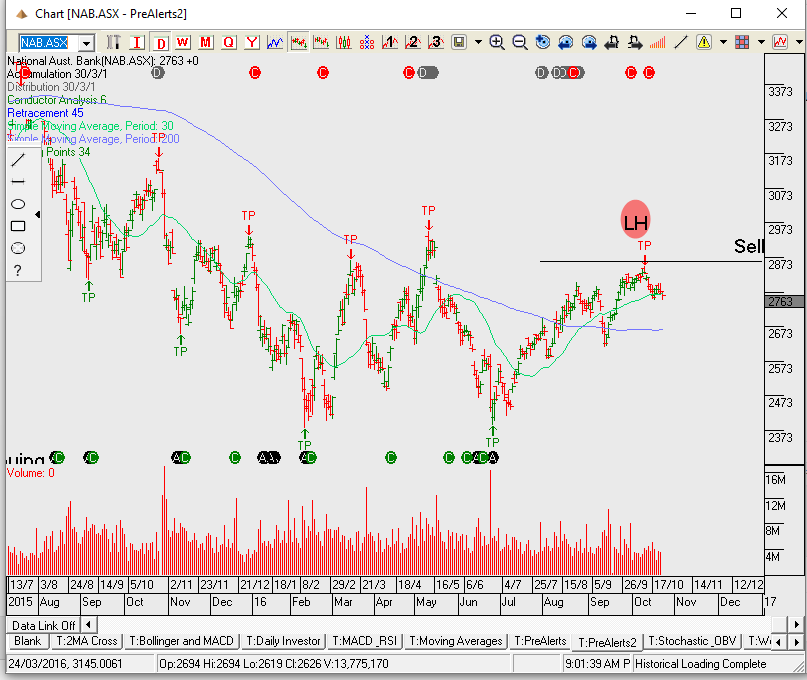

NAB is scheduled to report its FY16 result on Thursday and we’re expecting FY16 cash earnings of $6.4b. The final dividend will likely be around $0.98 fully franked & we continue to expect the dividend to be cut next year.

We are forecasting a 2H16 credit impairment charge of $500m which is an increase of $125m on the 1H16 number.

Based on a slight reduction in dividends the FY18 yield is 6.75%.

Selling covered calls at or near $28.50 into early next year, with a view towards collecting the upcoming dividend is our preferred strategy.

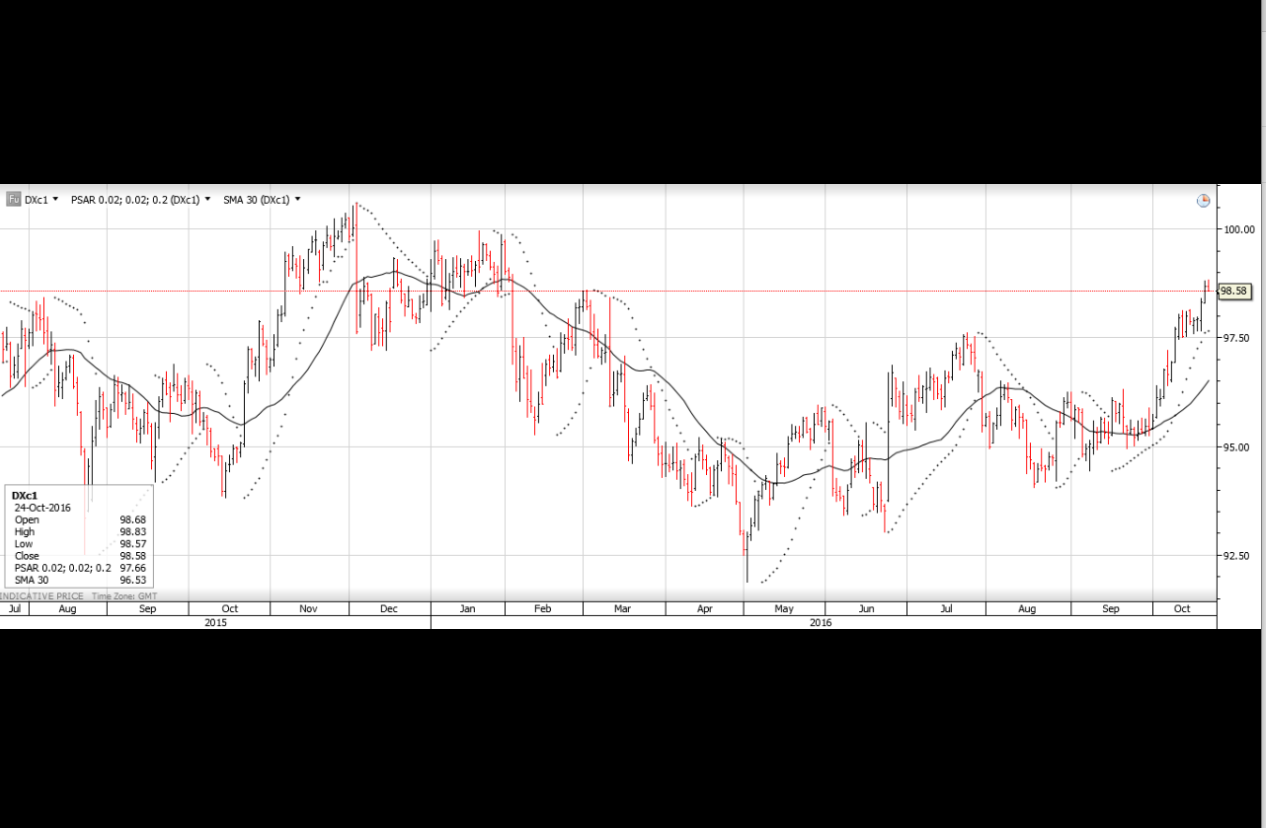

The USD ended on a firm note last week as foreign exchange traders were focused on the divergence of monetary policy between the Greenback and the other G-7 currencies. Over the last several trading sessions, we learned that European Central bank is still open to more stimulus in December, the Australian economy is not as vibrant as the RBA suggests and that the Reserve Bank of New Zealand is thinking about easing again before the end of the year. We also learned that the U.K. economy is slowing at a time when US growth aggregates have been posting mostly stronger numbers for employment, housing and retail spending.

The steady flow of generally hawkish comments from FOMC officials stands in contrast to the dovish language coming from other central banks and has helped the USD Index reach an eight-month high just short of 99.00 at Friday’s NY close. It’s our base case that the likelihood for further interest rate normalization will increase over the next few weeks which will support the USD, keep the SP 500 index in a “buy on the dip” pattern and lift 10-year treasury yields back into the 1.95% area

With only a few first-tier fundamental data points scheduled for this week, It’s worth looking at some of the technical price patterns which have emerged over the last several trading sessions. The most prominent technical pattern is the “Golden Cross” in the USD Index. A Golden cross is formed when the 50-day moving average crosses above the 200-day moving average and suggests a continuation to higher levels. We note that the last time this pattern emerged, the USD actually consolidated for a couple of weeks before moving higher. With US Durable Goods orders scheduled for Thursday and GDP to be released on Friday, the consolidation phase could be much shorter this time.

Since the Euro currency makes up close to 58% of the weighting of the USD Index, it’s not surprising that the same moving average time frames have crossed to the downside in the EUR/USD. This pattern is called the “Deadman’s Cross” and suggests last week’s break of the July trend line will see downside range extension this week.

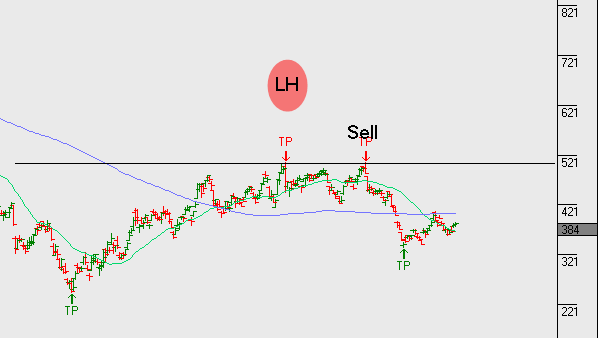

Most property stocks have broken their long term uptrends and are displaying the early signs of a “rollover” type pattern. We’ll most likely see a bounce from the current oversold level, driven from an outcome on the December Fed rate hike. However, the probability of a bearish lower high in the next 3 to 6 months will mean the counter trend trade from the current lows will be short and explosive but the real opportunity to watch will be the short side trade in 2017.

The above picture applies to most property trusts and property development companies. The exception appears to be SGP and LLC. Out of the two names, my preference remains Lend lease.

FY17 should deliver EBITDA of $1.2b, EPS of $1.30 and DPS of $0.68 placing the stock on a forward yield of 4.9%

Santos Energy Group (STO) report a sharp rise in Q3 production and sales allowing the company to re-calibrate its forward guidance to the top end of the range.

For the three months ending September 30, Santos posted a 31% increase in sales volume to 21.3 million barrels of oil while forward production advanced 7% to 15.5 million barrels. Sales volumes are anticipated to hit 81-83 million barrels for the full year.

Overall LNG sales volumes more than doubled to 1.3 million tons as the ramp-up of the company’s cornerstone GLNG project in Queensland accounted for 755,000 tons and shipping 21 cargoes in Q3.

Investors who were looking for specific details about the future trajectory of monetary policy from yesterday’s European Central Bank (ECB) press conference would have been sorely disappointed. Granted there was very little consensus that there was going to be any new policy measures announced, but ECB chief Mario Draghi and his staff still managed to fall short of even the lowest expectations. This lack of substance is best illustrated by the fact that Mr Draghi’s prepared statement at the beginning of the press conference, which usually run for 15 to 20 minutes, lasted less than five minutes.

However, Mr Draghi said nothing to dampen expectations that the new staff forecasts in December would support the extension of the of the current asset purchase program past the current expiry date of March 2017. This assessment is based on two economic realities: First, there are no convincing signs of an upward trend in Euro zone inflation. Second, growth risks in Europe’s largest economies are skewed to the downside. European equity markets were happy with Mr Draghi’s dovish tone as both the French CAC and German DAX both posted fresh two-month highs at 4557 and 10,750 respectfully.

The Euro has responded accordingly with the EUR/USD dipping below the 1.0900 handle for the first time in over four months in today’s Asian session. Reading between the lines of the ECB statement, it’s likely that December will be the time when the asset purchase program is extended by at least six months and the asset pool will be expanded. In contrast, recent comments from FED Governors Fischer and Dudley keep the prospects of further rate normalization in the USA very much on the table.

RIO’s 3Q16 production result was mixed. Copper production was weaker than expected & iron-ore shipments were broadly in line with market expectations. Thermal coal & coking coal delivered strong production numbers.

FY17 forecast revenue of $35b, EBIT of $5.5b, EPS $2.00 and DPS of $1.10, places the stock on a forward yield of almost 3%.

RIO.ASX

Send our ASX Research to your Inbox

Or start a free thirty day trial for our full service, which includes our ASX Research.